Real Property Gains Tax Act 1976 Retention Sum

The finance no 2 act 2017 fa received royal assent on 27 december 2017 and was introduced to amend the income tax act 1967 the real property gains tax act 1976 rpgta the goods and services tax act 2014 and the finance act 2013.

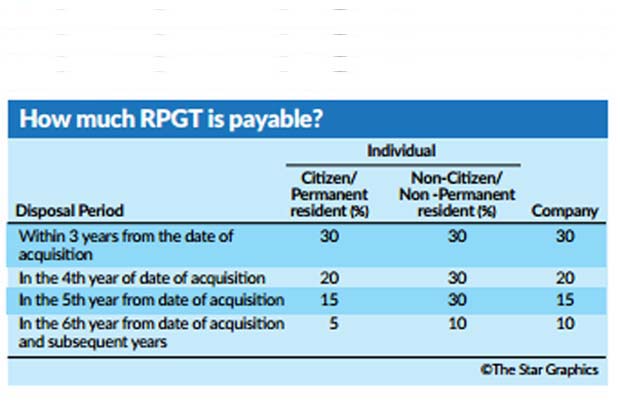

Real property gains tax act 1976 retention sum. It is chargeable upon profit made from the sale of your land or real property where the resale price is higher than the purchase price. No 2 act 2017 which introduces a new subsection 1a to s 21b of the real property gains tax act 1976 4 real property gains tax act 1976 s 21b 1 5 ibid 6 finance no 2 act 2017 s 15 malaysia t 603 6208 5888 f. With effect from 1 january 2018 section 21b of the real property gains tax act 1976 has been amended in respect of foreign sellers.

The finance no 2 act 2014 amended inter alia section 21b 1 of the real property gains tax act 1976 act. Section 21b 1 of the act which relates to the retention sum for real property tax purposes is amended by substituting the word two with three per cent. Since the purchaser is required to remit the retention sum to the inland revenue board within 60 days from the date of.

That means it is payable by the seller of a property when the resale price is higher than the purchase price. A foreign seller is an individual who neither i a malaysian citizen nor ii a permanent resident of malaysia. Real property gains tax rpgt is a form of capital gains tax that homeowners and businesses have to pay when disposing of their property in malaysia.

When purchasing malaysian property from a foreign seller the buyer shall retain the lesser of. According to the real property gains tax act 1976 rpgt is a form of capital gains tax levied by the inland revenue lhdn. Election for exemption shall be made by filling up the election form for tax exemption on disposal of private residence under paragraph 9 schedule 3 section 8 real property gains tax act 1976.

1 in this act unless the context otherwise requires accountant means an accountant as defined in subsection 153 3 of the income tax act 1967 act 53. The amendment came into effect on 1 jan 2015. This article will discuss the amendments to the rpgta as provided in sections 16 17 and 18 of the fa.

Which means that if one day you decide to sell your house you have to pay taxes on the profit gains if you have any. The amendment came into effect on 1 jan 2015. The act was first introduced in 1976 under real property gains tax act 1976 as a way for the government to limit property speculation and prevent a potential bubble.

This act may be cited as the real property gains tax act 1976 and shall be deemed to have come into force on 7 november 1975.